In late December of 2022, TIAA released the second of their annual reports on plans to address risks due to climate change. The first report, issued on December 24th 2021, was timed for maximum invisibility and was widely panned by educators, financial analysts, TIAA clients, think tanks and climate researchers for their lack of specifics and focus on very limited portions of TIAA’s overall assets.

In this analysis TIAA-Divest! reviews TIAA’s 2022 report to determine if TIAA and their asset manager Nuveen have improved their approach to managing the climate crisis.

Summary

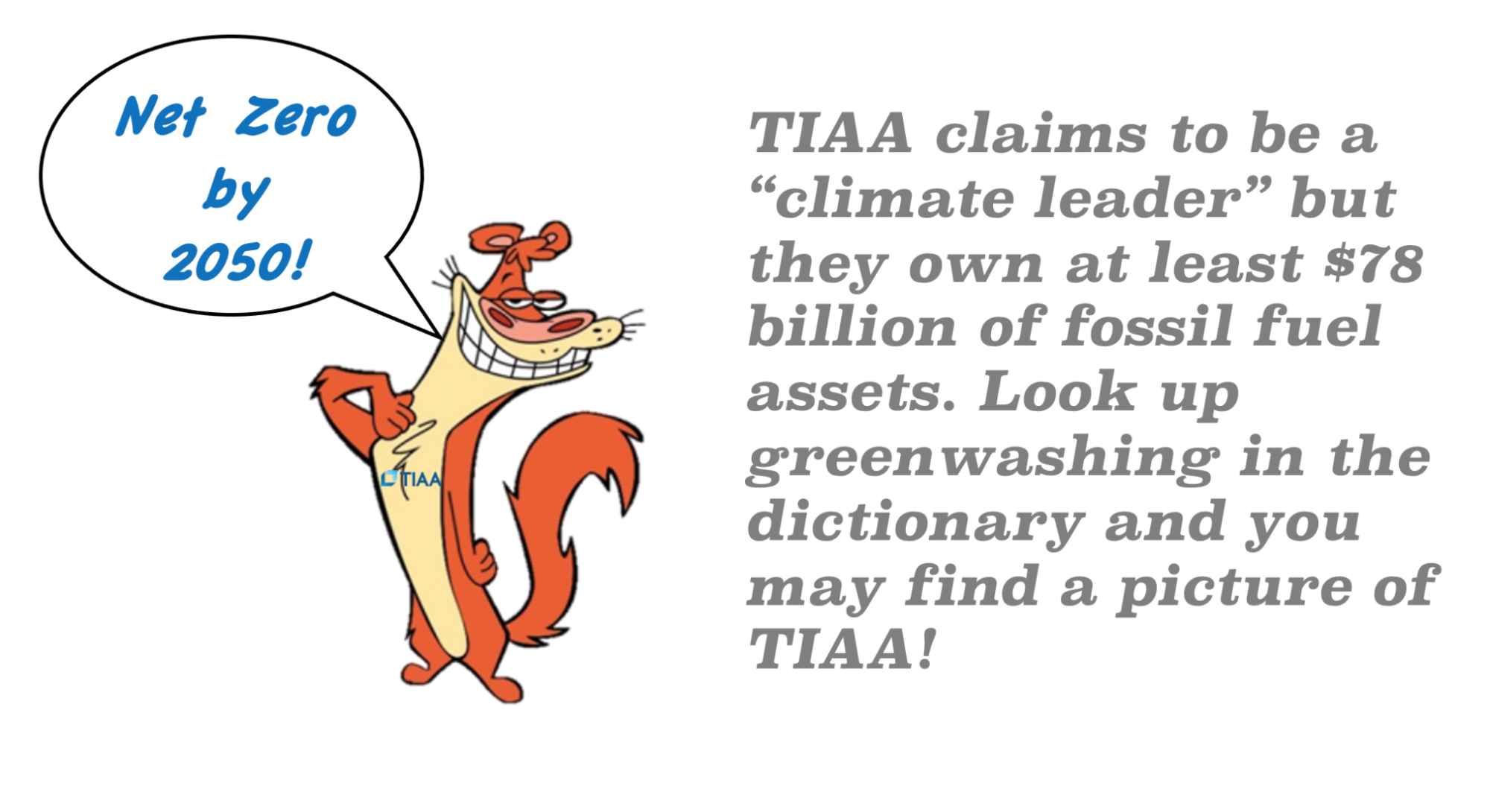

Despite the ongoing increase in deadly and destructive climate-driven floods, fires, heat waves, storms and droughts, TIAA’s 2022 Climate Report shows no improvement over their 2021 report. It is essentially deceptive, lacks meaningful targets, and uses language intended to cover up and defend, rather than to explain and clarify, TIAA’s has least $78 billion in fossil fuel investments; TIAA lags far behind their peers in their climate policy; TIAA is the world’s 5th largest holder of coal bonds and 10th largest holder of oil and gas bonds. In reviewing TIAA’s report, we found the following:

TIAA’s 2022 Climate report excludes the term “fossil fuels”. The connection between fossil fuels and climate change is never mentioned and decarbonization is never presented as one of the company’s goals.

TIAA has limited the scope of their climate efforts to their real estate assets and to their general fund account. They continue to ignore their total Assets Under Management, for which there are no climate targets whatsoever.

TIAA relies heavily on offsets in their to achieve a net-zero carbon profile for the assets they have chosen to consider. We find this problematic and disingenuous for reasons we describe in detail below.

TIAA’s target date of 2050 to achieve net-zero emissions, with no interim targets, is too little and much too late. TIAA must begin to address the climate impacts of their investment strategy immediately if they have any hope of contributing meaningfully to the low carbon transition.

TIAA-Divest! conferred with financial experts as part of our review. These experts without exception found TIAA’s report to be mostly window dressing, containing very little of substance with regard to TIAA’s approach to climate change.

Overarching Themes

The TIAA 2022 climate report is broadly divided into four major sections. Governance, Strategy, Risk management and Metrics & Targets.

The governance section attempts to describe how TIAA’s very complex management structure will divide the work of addressing climate risk across multiple layers of management and various governing bodies including the Board of Trustees, an “ESG council”, the Responsible Investing Team and other TIAA and Nuveen departments.

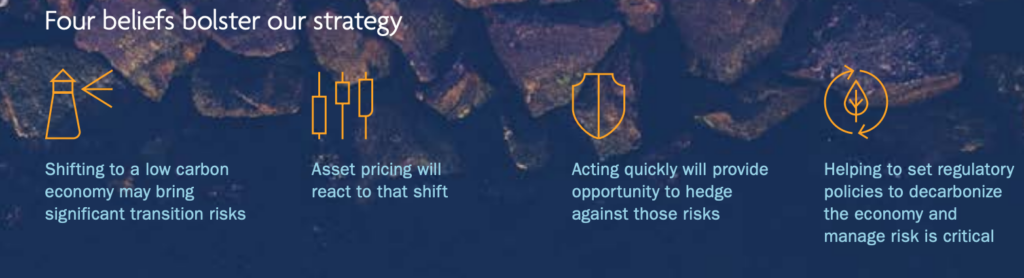

The Strategy section discusses some of the plans TIAA/Nuveen has developed to deal with the challenges posed by climate change. In this section, TIAA lists four “climate beliefs” that underpin their climate strategy. The remainder of this section seeks to shed light on the risks, opportunities and strategic actions associated with each of the beliefs and also provides pages intended to demonstrate that TIAA understands climate risk and that they are equipped to manage that risk.

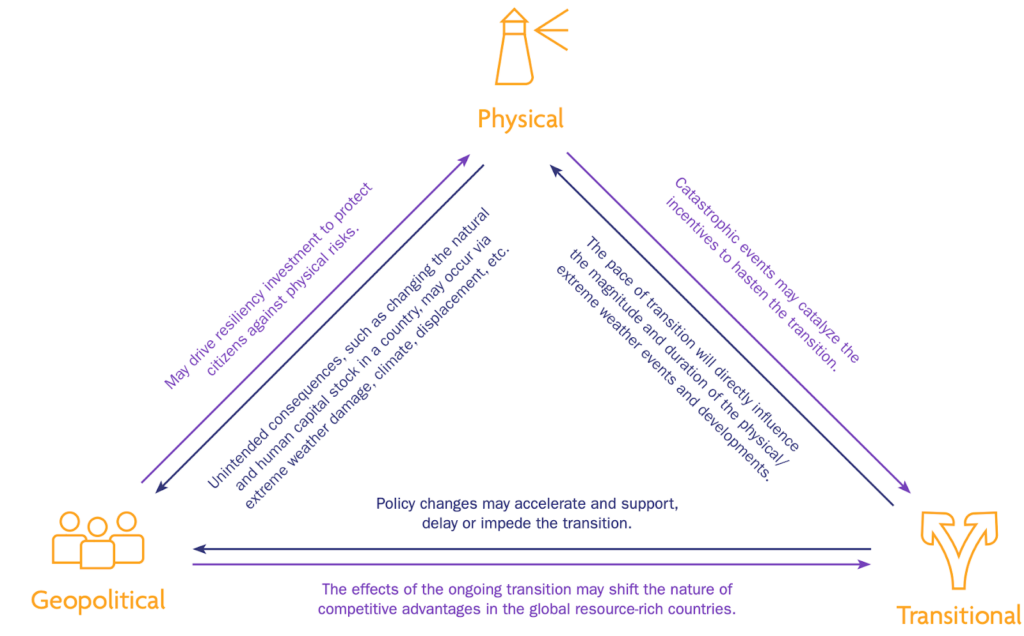

Risk Management is covered on a single page. Here, TIAA tries to explain the geopolitical aspects of climate change in a single triangular chart which purports to show how “physical,” “transitional” and “geopolitical” forces influence one another. These terms are not defined, but it appears that “physical” refers to infrastructure and the natural world whereas “transitional” refers to the risks associated with transitioning away from a carbon economy.

Metrics and Targets consumes more pages (8) than any other section. The climate impacts of TIAA’s operations (offices, cafeterias, travel, etc) and TIAA’s real estate assets are the focus and it is clear that TIAA has much more to say here as compared with the climate implications of their investment decisions.

Analysis of section I, Governance

TIAA has correctly been called a behemoth. It is a huge organization, comprising dozens of subsidiaries and divisions spread across the United States, so it is not surprising that TIAA’s internal structure should be confusing to outsiders. However TIAA seems to have made an extra effort to obfuscate the division of responsibilities across operational units.

Near the top of the hierarchy sits the TIAA Board of Trustees, a body that incorporates a number of committees which have overlapping responsibilities for “design and implementation” of climate risk strategy. The success or failure of TIAA’s climate strategy will depend on how well the trustees do their job. Perhaps the most interesting revelation on the page devoted to Board of Trustee responsibilities is the reference to the “climate risk framework,” for which the Risk and Compliance Committee has oversight. The climate risk framework is intriguing because it appears to represent the ultimate expression of TIAA’s climate ambitions. However, our attempts to identify any documentation or other description of this framework have not borne fruit. We were able to locate a Nuveen case study, “A climate risk framework for farmland investments” that was prepared for the PRI (See here XXX for TIAA-Divest’s disappointing experience with PRI). but we found nothing in this case study that would provide a roadmap for a coherent climate strategy.

Mysterious “frameworks” appear to be a hidden theme of TIAA’s climate report. In addition to the missing climate risk framework, TIAA points to the “net zero framework,” “the data infrastructure, risk and governance frameworks,” and “Nuveen’s Global Fixed Income impact framework.” If any of these frameworks actually exist, TIAA has kept them well hidden, leaving us to wonder if TIAA understands that transparency is one of the core principles of responsible investing.

Analysis of section II, Strategy

TIAA’s strategic approach to the climate crisis is built on “Four beliefs”:

Shifting to a low carbon economy may bring significant transition risks

Asset pricing will react to that shift

Acting quickly will provide opportunity to hedge against those risks

Helping to set regulatory policies to decarbonize the economy and manage risk is critical

“If TIAA can manage their investments in such a way that they come out ahead financially, then apparently extinctions, floods, fires and refugee crises are not an impediment.”

Here we can see how an asset manager’s approach to climate change differs from that of scientists, policy experts and NGOs. Where the latter are concerned with minimizing the natural and human impacts of climate change by working to keep global temperature rise below 1.5C, TIAA approaches climate change from a strictly transactional perspective. If TIAA can manage their investments in such a way that they come out ahead financially, then apparently extinctions, floods, fires and refugee crises are not an impediment. This is at odds with CEO Thasunda Brown Duckett’s introductory message in which she expresses the following sentiment: This work is critical as many of us increasingly feel the impacts of climate change in our own lives. This year we’ve seen deadly floods from South Africa to Kentucky, heat waves in India, Pakistan and Europe, and drought in eastern African countries such as Ethiopia, Kenya and Somalia.

TIAA devotes a page to each belief, reviewing risks, opportunities and strategic actions. For belief 1, Shifting to a low carbon economy may bring significant transition risks, TIAA identifies risks associated with a low carbon transition coming from regulatory, technological and market changes. While TIAA provides few details for transition risk, we have seen them deliver consistent messaging which indicates that they view transition risk as financial uncertainty. Because it is not possible to predict (in large part because of government and industry inaction) exactly what form the low-carbon transition will take, TIAA’s appears to be unable to shift their focus away from the traditional energy sector. As a result, TIAA exposes themselves to a greater risk originating from the loss of value in this sector, as coal, oil and gas are quickly phased out. In some cases, TIAA will be left holding “stranded assets” which are those where liabilities exceed value. We have seen TIAA face this reality recently when they became the majority owners of several obsolete power plants after the owner declared bankruptcy.

Opportunities arise when companies are able to adapt quickly to the risks leading to business advantage. TIAA’s strategic actions include investing to “outperform in a low carbon transition” and prioritizing “companies and assets that… will benefit from the low-carbon/net zero transition.” To date, we have seen no indications that TIAA is executing this strategy; in fact they continue to devote increasing amounts of capital to fossil fuel investments. One way to reconcile the disparity is that TIAA is hedging their bets on climate so that they come out ahead regardless of whether the low-carbon transition succeeds or fails, an approach consistent with TIAA’s single focus on returns. This narrow vision allows TIAA to justify exacerbating the climate emergency via direct injections of cash while ignoring the negative impacts on their customer’s lives which TIAA considers to be “externalities.”

Belief 2, Asset pricing will react to that shift, finds risk in the possibility that “An abrupt or disorderly low carbon transition is expected to increase the transition risk facing… investments with exposure concentrated in fossil fuel and energy intensive sectors.” Again, TIAA views the financial risk to investments as paramount, while environmental and societal disruption are ignored. TIAA finds opportunity in “Green sectors [which] may benefit significantly from a low carbon transition”; however, the strategic actions identified do not include moving investments from carbon-intensive sectors to renewable energy. Instead the actions include “offer[ing] clients a variety of low carbon and climate-focused products” and “work[ing] with assets, portfolio companies and other stakeholders in carbon intensive industries to help support them in their low carbon transition.” The first is disingenuous in that even the TIAA-CREF Social Choice Low Carbon Equity Fund is heavily invested in fossil fuels, and the second allows TIAA to push responsibility for emissions to their portfolio companies without any leverage to ensure that such transitions actually occur.

Belief 3, Acting quickly will provide opportunity to hedge against those risks, receives less attention, identifying regulatory changes as a risk, carbon trading as an opportunity and building frameworks as strategic actions. TIAA-Divest is particularly concerned that TIAA is looking at carbon as “an investable asset class”. TIAA owns millions of acres of land in Brazil and the US which are being damaged by industrial farming and conversion of wild lands for cattle grazing, wood chips and other environmentally unsound practices. TIAA’s entry into carbon trading markets is likely to accelerate the destruction of these lands and further damage nature’s ability to sequester carbon via natural processes.

Belief 4, Helping to set regulatory policies to decarbonize the economy and manage risk is critical, identifies lack of transparency on emissions by companies as a risk and the possibility that this condition may improve as an opportunity. Ironically, TIAA has resisted disclosing the emissions resulting from their own investment choices. As an example, TIAA is one of the largest lenders to Adani Enterprises, an Indian coal conglomerate that generates billions of tons of greenhouse gas emissions. TIAA has failed to release the details of these investments, making their statements here hypocritical at best.

Analysis of Section III, Risk management

It is not clear exactly what point TIAA is trying to make about climate risks other than that they are complex and that facing these risks requires paying attention to multiple factors. What is apparent is that TIAA appears to be unprepared to manage their $1.4 trillion in assets in a way that ensures the end result is not only profitability, but also improves, or at least does not exacerbate the climate crisis. A proper strategy for managing climate risk would be forward looking and would recognize that investors can alter the outcome by treating their decisions as an integral part of the success or failure of the 1.5C pathway.

Analysis of Section IV, Metrics and targets

TIAA discusses four targets for reducing carbon emissions. They are:

i. Operational emissions: Net Zero by 2040

ii. Operational emissions reduction measures

iii. Nuveen Real Estate emissions: Net Zero by 2040

iv. General Account: Net Zero by 2050

Targets i-iii fall under the category of emissions for which TIAA has direct control. For example, operational emissions are those associated with TIAA’s regular business operations. That includes everything from the electric power used for heating and lighting TIAA’s offices, corporate travel, and waste disposal. TIAA intends to reduce their net operational emissions to zero by 2040 and they claim that they are already making significant progress towards that goal. TIAA also intends to bring Nuveen’s substantial ($156 Billion) real estate holdings to net zero by 2040.

These efforts are laudable and we don’t doubt that TIAA can achieve them. However it is important to note that TIAA is not aiming for zero emissions. They are aiming for net zero emissions. Where TIAA can’t eliminate emissions, they “will neutralize the remaining emissions through carbon sequestration by purchasing verified carbon offsets from approved voluntary carbon offset registries”. At this time carbon capture and sequestration is an unproven technology for which all pilot projects have proven infeasible. If TIAA is referring to sequestration via agriculture or other nature-based approaches, we have reason for concern. TIAA has demonstrated that they are poor stewards of the land and every land-based initiative they have embarked on has produced results worse than if TIAA had simply left the land alone. TIAA is not to be trusted if they plan to implement their own carbon sequestration effort.

TIAA’s reliance on “approved voluntary carbon offset registries” is also problematic. Recent investigations by major news outlets have shown that more than 90% of rainforest carbon offsets by the largest providers are ‘worthless’ and that claims corporations relying on offsets to achieve net zero goals are often exaggerated or based on incorrect assumptions.

TIAA touts their goal of having their general account reach net zero carbon emissions by 2050. The general account is a collection of assets worth approximately $300 billion that backs TIAA’s annuities and other “insurance” products. While the general account is a substantial portion of TIAA’s assets, it does not comprise the majority of TIAA’s assets, which are not covered by a net zero target.

As described above, we don’t buy the net zero approach as there are too many opportunities for unscrupulous operators to market false offsets, obscuring real emissions that can only be addressed by real solutions. We also believe that the arbitrary 2050 target date is a distraction, allowing TIAA’s decision-makers to operate in a business as usual manner while their successors will be left to clean up the mess. Current climate models require that all new fossil fuel development needs to end now, and what is TIAA but a means for companies to develop their business via outside investment. The combination of net-zero by 2050 with no plan to exclude investments in coal, oil and gas clearly indicates that TIAA will not be making any meaningful changes to the emissions profile of their investments before it’s too late for changes to make a difference.

Conclusion

With assets under management of $1.2 trillion, TIAA invests more money than many countries generate in GDP. TIAA paints themselves as concerned about climate and the environment, but their investment decisions demonstrate that these concerns are not reflected in their business model. TIAA has over $78 billion invested in coal, oil and gas projects placing them among the worst retirement providers in terms of environmental responsibility

Over the past two years, in response to pressure from groups like TIAA-Divest! We have seen TIAA release two climate reports, both entitled “ensuring our future”. These reports, the only publicly available description of TIAA’s strategy for addressing the climate crisis generate more questions than answers. There is no clarity to how exactly TIAA will zero out the emissions generated by their investment portfolio nor any timeline other than “by 2050”. These reports refer to various entities and frameworks that are not described anywhere. TIAA tries to defer responsibility for investing in fossil fuel projects by claiming that companies are not stringent in their reporting, while ignoring the obvious fact that investing in a coal or oil company encourages additional coal and oil development.

After reviewing TIAA’s climate reports as well as investigating TIAA’s fossil investments, their lack of transparency and their unwillingness to engage with their customers who demand an end to financing the climate emergency, TIAA-Divest! has concluded that TIAA will only change when forced to do so. We welcome those whose retirement savings are being managed by TIAA to join us so that our retirements will not come at the expense of future generations.